Fiscal dominance: when the body attacks itself

A country dives into fiscal dominance when concerns about government debt start “dominating” everything else - like an autoimmune disease that starts attacking the body’s own organs. An economy suffering from fiscal dominance starts to lose control of its healthy functions one after another.

The first casualty is monetary policy as central bank finds it exceedingly difficult to set interest rates independently. Central bank is “forced” to set interest rates high in order to defend the currency against fiscal solvency concerns and/or limit inflation from money printing. As a result, the country loses monetary independence, which is a huge loss.

The second casualty is the financial sector. A healthy financial sector play a key role in financing private investment. But fiscal dominance burdens the financial sector with high interest rates due to the loss of monetary independence. Fiscal dominance also comes with financial repression, as governments strong-arm the financial sector into holding government bonds. Both the high cost of financing and financial repression restrains the financial sector from financing private investment and hence growth.

The third casualty is a wider loss of confidence and consequently a broader “run” on the economy. Investors and workers do not feel confident about long-term viability of the country’s financial future and flee to other places around the world.

And as they say, three strikes and you are out. So which countries in the world are most crushed under the weight of fiscal dominance today?

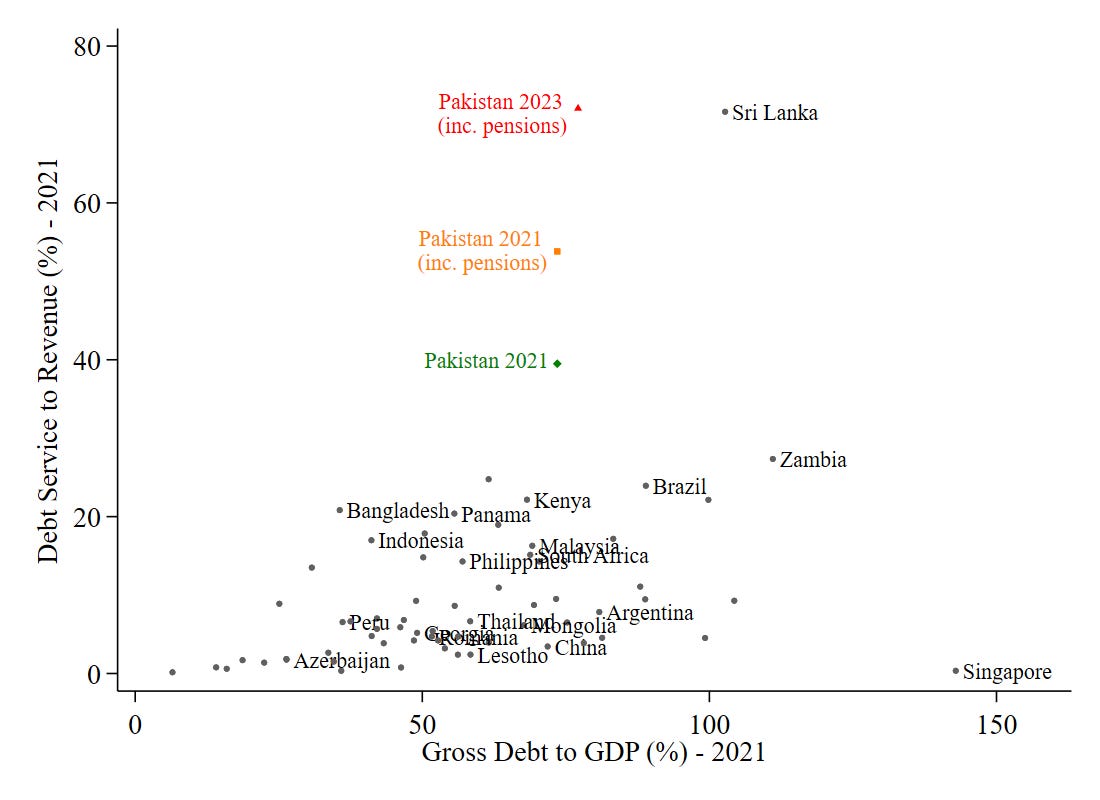

The figure below ranks countries according to the share of government revenue that goes into servicing debt - a measure of the extent of fiscal dominance. The latest available year with sufficient coverage of developing countries is 2021. Sri Lanka stands out the most, and its a country that has already declared default since 2021.

The next country facing extreme fiscal dominance is Pakistan (the green dot). Pakistan’s debt service to revenue ratio is significantly higher than all other countries, but even this understates the true extent of Pakistan’s fiscal dominance woes. The orange dot adds the unfunded pension debt service that the government must pay every year. Pakistan’s government has promised pensions to its military and civilian workforce without funding these through contributions. These unfunded pension liabilities thus effectively add to Pakistan’s total debt.

Pakistan’s extremely high debt service ratio makes it susceptible to self-fulfilling runs that I mentioned earlier. This danger came to the surface during the 2022-24 crisis when central bank *had* to raise rates (that is the definition of fiscal dominance). The red dot shows the sharp jump in debt service ratio as a result of this rate rise.

Finally, even the red or orange dots do not fully reflect the true extent of Pakistan’s fiscal dominance challenge. The reason is that in another example of very poorly thought out policy decision, Pakistan chose to essentially bankroll its entire power sector with sovereign guarantees (this is why i say the nervous system is broken). As a result, Pakistan has a zombie power sector that is loaded with bad sovereign debt. It is a bit of a technical issue how to add this debt service in the figure above, but my back of the envelope calculation suggests that it should be of similar magnitude as the country’s unfunded pension liabilities.

The bottom line is that the combination of Pakistan’s domestic debt, external debt, unfunded pension liabilities and zombie power sector has pushed Pakistan into an extreme form of fiscal dominance - hard to think of any other country that is in as bad a shape. The lesson for other countries is: be afraid of fiscal dominance, and put checks in place beforehand to guard fiscal health.

(PS: I am using consolidated government revenue to calculate Pakistan’s debt service to revenue ratio. Since more than half of federal revenue goes to the provinces - and is not used to service the debt, debt service to net federal revenue number is much worse. It would be more than 100% with pensions included.)

Brief Solution

1. Fiscal Consolidation:

Reduce unnecessary government spending, enhance tax collection, and restructure existing debt to manage financial obligations more effectively.

2. Pension Reform:

Fund pensions through sustainable contributions, cut future liabilities, and shift to more sustainable pension models.

3. Monetary Policy Independence:

Strengthen the central bank’s autonomy to set interest rates independently, focusing on inflation control and economic stability.

4. Revitalize Financial Sector:

Reduce mandatory government bond holdings by banks to minimize financial repression and encourage private sector lending.

5. Power Sector Reform:

Address inefficiencies, restructure debt, and reduce government guarantees. Publicize power sector agreements with Independent Power Producers (IPPs) to expose and address hidden costs, as IPPs receive payments even without generating power.

6. Build Confidence:

Improve governance, enhance transparency, reduce corruption, and implement broad economic reforms to restore investor confidence and stabilize the economy.

These actions aim to reduce fiscal dominance, improve public accountability, and restore economic control.

May I request your comments and thoughts on the solutions to cure the extreme case of Fiscal Dominance? Solutions are obvious but please share your thoughts on an action list using priority and stakeholder impact.